Owning the same residential home for many years or decades has been shown to be less costly to the resident versus renting over the long-term. However - real estate is also frequently advertised as an “investment” or a “diversifier” in a portfolio of financial assets.

The definition of an ”investment” is an asset that increases money or purchasing power over the long-term, and real estate is advertised as such.

Millionaires and multi-millionaires know better.

From Thomas Stanley’s bestselling The Millionaire Next Door:

“…as I mentioned in Stop Acting Rich, 64% of the millionaires surveyed never owned a vacation home, beach bungalow or mountain cabin, not even a lean-to or a tree hut in the woods.”

In truth real estate can, slowly or quickly, destroy an investor’s purchasing power, create liquidity crises and increase portfolio risk substantially over an investor’s lifetime.

Money is defined as “purchasing power”. Here’s how real estate drains your money over time:

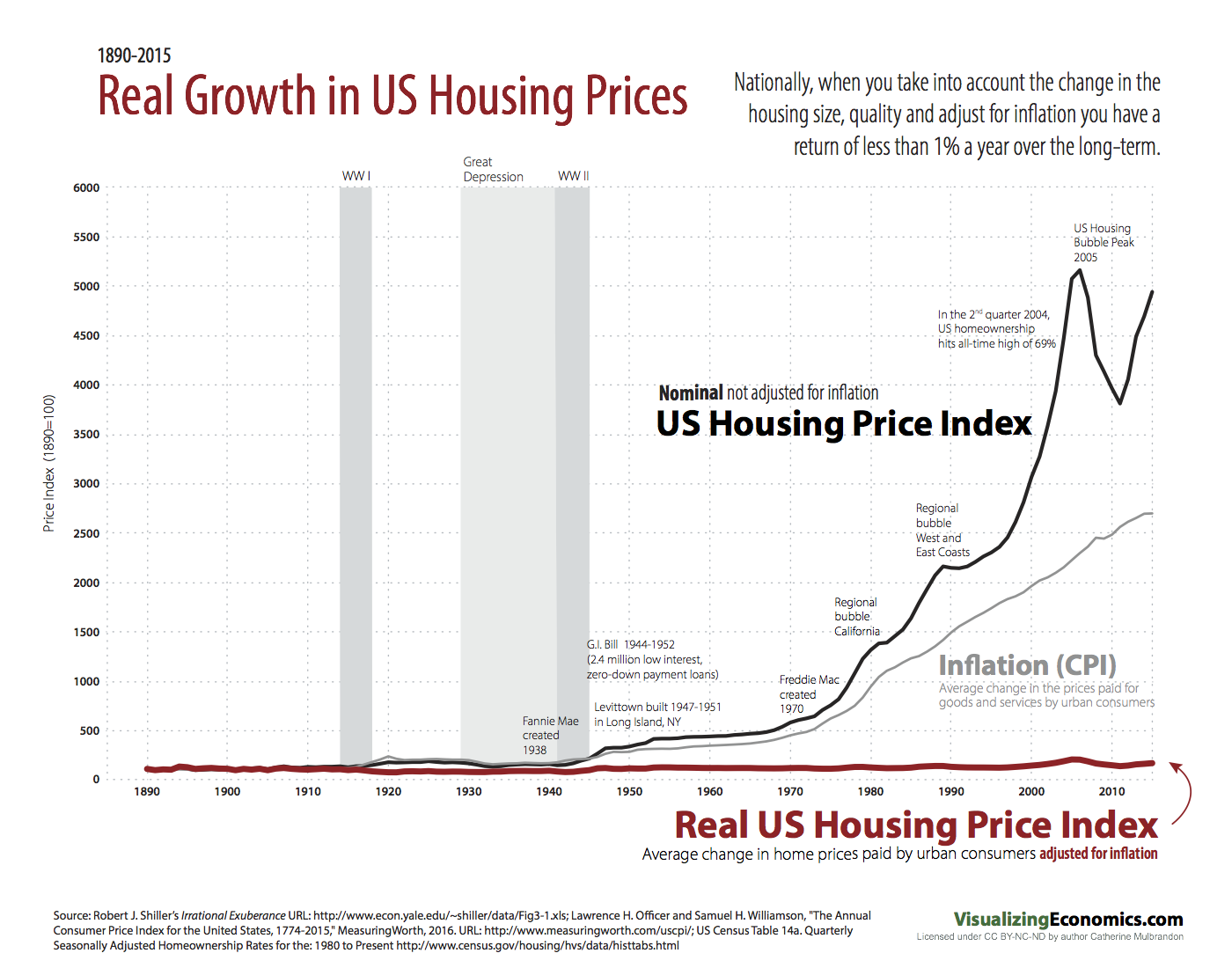

+4%. Historical annual return Single Family Home per Robert Shiller (Case/Shiller Housing Index)

-3%. Average annual inflation rate

-1.1%. Average annual property tax expense

-.5% Average annual property insurance expense

-1.5% Average annual property repairs and maintenance expense

-2.1% Total Average annual loss in purchasing power - single family home

Link: Real Estate Investment Performance

By itself, it's very difficult for an investor to ever have a diversified portfolio of real estate. Most holdings become pieces of a few similar assets (condominiums, apartment houses, office buildings) in the same areas. The result is often under-diversifying, both by location and by property type. Here are some important facts:

1. It is a myth that one's home provides a significant growth of capital. Since 1945, American single family home prices have risen at a rate of about 4% per year. (Case-Shiller Index - Nobel laureate Robert Shiller). So after inflation, Net return on property has totaled about 1% per year. By comparison, the return of the S&P 500 index has been about 10% (Net 7%) per year - a return which requires no maintenance, repairs or tenant vacancies.

2. The advertised returns of real estate usually rely on high leverage, which increases risk significantly. The loss of a tenant, or their financial distress can force a leveraged property into negative cash flow which the investors may be liable.

3. Real Estate is by nature illiquid, costly to buy and sell, and requires time and effort to manage effectively.

4. Local laws/legislation and tax policy can regulate rents and restrict a landlord from evicting tenants.

If there is an insistence to own a large percentage of real estate, there are options to avoiding risky concentration such as a diversified Real Estate Investment Trust. However REITs still have liquidity restrictions and the properties in them still mirror historical real estate returns of annualized 1% Net (versus 7% Net annual returns for owning equity in 500 of the largest companies of the world).

(Sources: Nick Murray, Robert Shiller)

http://www.econ.yale.edu/~shiller/data.htm

https://wealthtrack.com/robert-shiller-nobel-prize-winning-economist/

https://awealthofcommonsense.com/2013/03/real-estate-investment-performance/

New York Times:

April 13, 2013

WHAT prices will today’s home buyers get if they sell a decade from now?

Most people live in their home for many years. They don’t need to view it as an investment at all, but if they do, they surely need a long forecasting horizon.

The problem is that modern economics has a poor understanding of past movements in home prices. And that makes the task of predicting the state of the market in 2023 challenging, at the very least. Still, we can learn something by analyzing the factors that affect home prices in general.

There has been some good news lately: home prices have risen over the last year, and with those gains there has been a renewed sense of optimism. But do these price increases mean that homes are now good investments for the long haul?

Unfortunately, no. We do know one thing from economic research: one-year home price increases, after correcting for inflation, have had almost no statistical relationship to increases 10 years down the road. Thus, the upturn last year is irrelevant to long-run forecasting. Booms are typically followed by busts, usually in far less than 10 years. In a decade, an entire housing boom, if there is one in inflation-corrected terms, is likely to have been reversed and completely washed away.

Inflation has a major impact on long-term home prices. So do the costs of construction. We’ll examine these factors now, and turn to other important influences like speculative pressures and cultural and demographic trends in subsequent columns.

Home prices look remarkably stable when corrected for inflation. Over the 100 years ending in 1990 — before the recent housing boom — real home prices rose only 0.2 percent a year, on average. The smallness of that increase seems best explained by rising productivity in construction, which offset increasing costs of land and labor.

Of course, home prices are likely to be much higher in 2023 when measured in nominal dollars — those that aren’t inflation-adjusted. Inflation is the deliberate policy of the Federal Reserve, with a target rate now of 2 percent a year as measured by the personal consumption expenditure deflator, or about 2.4 percent on the Consumer Price Index. At those rates, nominal prices will be roughly 25 percent higher, over all, in a decade.

All else equal, the current Fed policy would have this effect: a home selling for $200,000 today will sell for around $250,000 in 2023, though the real price — corrected for inflation — would be unchanged. But because people often forget to correct for inflation, they may have the illusion that the market is improving.

In an ideal world, steady and uniform inflation would have no effect on rational decision-making because it affects incomes as well as prices. But in the real world, inflation does affect our psychology. People feel more optimistic when their nominal pay rises or when a neighbor’s house sold for more than they paid for theirs. But in thinking about investments for the long term, we should focus on fundamentals — on real, inflation-corrected values and on the economics behind them.

Here is a harsh truth about homeownership: Over the long haul, it’s hard for homes to compete with the stock market in real appreciation. That’s because companies whose shares are traded on a stock exchange retain a good share of their earnings to plow back into the business. The business should grow and its real stock price should also grow through time — unless the company makes poor decisions, as some certainly do.

By contrast, real home prices should decline with time, except to the extent that households shell out some money and plow back some of their incomes into maintenance and improvements, because homes wear out and go out of style.

Housing is an ambiguous investment to evaluate, because a good part of its real return typically comes in its providing a place to live, not in providing dividends paid in cash. For example, a homeowner may gradually realize that she doesn’t need all of the space in her house, but may not be emotionally prepared to start recapturing some of its economic value. The owner may not want to take in roomers, to use the old phrase, just as a modern renter may not want to live in a room in someone else’s home (though new markets like airbnb.com are aiming to change that mind-set).

Then there is the role of the construction industry, which is very good at building new homes and will crank out many more of them if prices rise relative to construction costs. It’s logical that homes’ ultimate values should be affected by home construction costs.

Ina 1956 study of home pricesby the National Bureau of Economic Research, Leo Grebler, David M. Blank and Louis Winnick documented a substantial decline in inflation-corrected construction costs per housing unit in the first few decades of the 20th century. They traced this decline to multiple causes, including a decline in the number of rooms per home, the use of gypsum wallboard in place of plaster and of asphalt shingles in place of slate, a shift in construction to lower-cost Southern climates and a relative increase in the number of multifamily housing units and apartment buildings. The authors concluded that the long-run movements in construction costs and home prices are “remarkably similar.”

This was the prevailing theory of home prices at the time: construction costs drove the entire housing market. That view — which implies that increasing productivity has restrained prices and could do so in the future — is very different from the focus on financial pressures and speculative bubbles that drives much of our thinking now.

Steady progress in developing new construction equipment, materials and techniques can be seen in something as simple as the history of power drills. A big step forward came in 1889, with the invention of the electric drill. Then came a series of other inventions: the portable electric drill in 1895, the pistol-grip-and-trigger-switch portable electric drill in 1917 (by S. Duncan Black and Alonzo G. Decker), the Phillips head screw in 1935 (by Henry F. Phillips), the first cordless electric drill in 1961 and the first lithium ion battery, which improved cordless drills, in the 1970s. Each set in motion a string of other improvements that, over decades, penetrated the construction industry and vastly improved its productivity. We can expect more such inventions in the future.

It is hard to imagine the next advances in home construction technology, but there are some clues. For example, Behrokh Khoshnevis of the University of Southern California is developing“contour crafting” roboticsthat he says will be able to accept computer instructions and, like gigantic 3-D printers, build houses. We cannot tell how well this will work, but computer technology has produced some amazing results. Why is it that we worry about the effect of information technology on our jobs but usually don’t link such uncertainty to the outlook for home prices?

Technical advances affect other industries, too, of course, and the performance of housing as an investment relative to others depends ultimately on the comparative rates of progress.

THESE variables alone suggest how tricky it is to forecast your home’s value when the time comes to sell. Prices can go down as well as up. That is also true for investments in general, of course, and is why generations of portfolio analysts have advocated assessment of risks, and not just extrapolation of recent trends, as the key to intelligent investing.